Cyber liability insurance explained: Learn about cyber insurance requirements, what does cyber insurance cover, and cyber insurance for small business owners.

June 23, 2026

.avif)

.avif)

.avif)

Cyber liability insurance is now a must-have for any business that handles customer data or uses digital systems. With the rise in cyber risk, breaches, and ransomware attacks, even small businesses face real threats to their operations and finances. This blog explains what cyber liability insurance is, how it protects your business, what is typically covered, and why it matters for small business owners. You’ll also learn about insurance policies, cyber insurance requirements, and practical steps for choosing the right coverage and managing insurance costs.

Cyber liability insurance helps protect your business from the financial impact of cyber incidents. These incidents can include data breaches, cyber attacks, and even mistakes made by employees that lead to a loss of sensitive information. If your business stores customer data, processes payments online, or relies on digital systems, this coverage can be essential.

Many insurance policies cover costs like notifying affected customers, hiring cybersecurity experts, and restoring lost data. Some policies also help with legal fees and regulatory fines. By having cyber liability insurance, you can focus on running your business, knowing you have support if a cyber event occurs.

Choosing the right cyber insurance coverage can be tricky. Here are some of the most common mistakes businesses make and how you can avoid them.

Many businesses think they are too small to be targeted, but cyber criminals often go after smaller companies with weaker defenses. Not understanding your true cyber risk can leave you exposed.

Not all cyber insurance policies offer the same protection. Some may only cover certain types of breaches or exclude specific cyber threats. Always review what is covered by cyber insurance before purchasing.

Focusing only on price can lead to gaps in coverage. Sometimes, a lower insurance cost means less protection or higher deductibles. Make sure you understand what you are paying for.

Some providers offer business insurance packages that include cyber liability insurance. Bundling can save money and make claims easier to manage.

If you experience a data breach, your cyber insurance requirements may change. Failing to update your policy can leave you without coverage for future incidents.

Certain industries have strict rules about data protection. Not checking your cyber insurance requirements against these rules can result in fines or uncovered losses.

Human error is a leading cause of cyber incidents. Some policies require regular cybersecurity training for staff. Skipping this step can void your coverage.

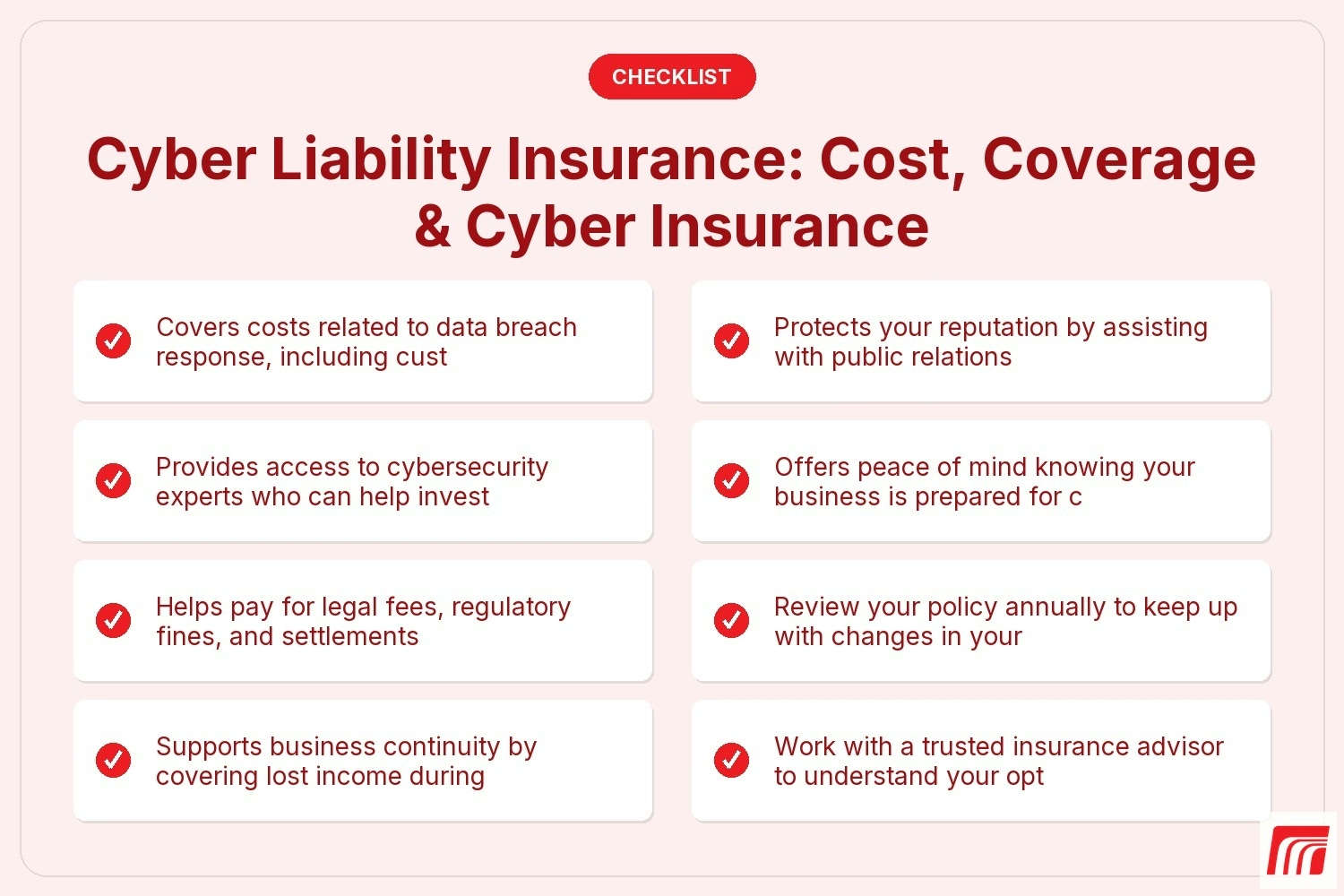

Having cyber liability insurance offers several important advantages:

Cyber liability insurance typically covers a range of incidents, including data breaches, cyber extortion, and cyber attacks. Most policies help pay for the costs of investigating a breach, notifying customers, and restoring lost or stolen data. They may also cover legal expenses, regulatory penalties, and even ransom payments if your business is hit by ransomware.

Some policies go further by including liability coverage for third-party claims, such as when a partner or vendor is affected by your breach. It’s important to review your policy details to understand exactly what is and isn’t included. This helps ensure you have the right protection for your business’s unique needs.

Selecting the right cyber insurance for small business owners involves several important steps. Here’s how you can make a smart choice.

Start by evaluating the types of data you handle and the systems you use. Businesses that store sensitive customer information or process payments online face higher risks and need broader coverage.

Look at multiple insurance solutions to see what each one offers. Pay attention to coverage limits, exclusions, and the types of incidents covered.

Some industries or clients require specific types of cyber insurance coverage. Make sure your policy meets these requirements to avoid compliance issues.

Balance the cost of cyber insurance with the level of protection provided. Sometimes, paying a little more can save you from major financial losses later.

If your business provides technology services, you may need technology errors and omissions insurance in addition to cyber liability coverage. This protects you from claims related to mistakes in your work.

Some insurers offer extra services, like cybersecurity training or risk management advice. These can help reduce your chances of a cyber incident in the first place.

Always review your policy documents carefully. Make sure you understand what is and isn’t covered, and ask questions if anything is unclear.

Once you have chosen a policy, there are a few steps to make sure your cyber liability insurance works for you. First, keep detailed records of your IT systems and data storage practices. This helps if you ever need to file a claim. Next, train your employees on basic cybersecurity best practices, since human error is a common cause of breaches.

Regularly review and update your insurance cover as your business grows or changes. If you add new services, hire more staff, or start handling different types of data, your coverage needs may change. Staying proactive helps ensure you always have the right protection.

To get the best value from your cyber liability insurance, follow these simple tips:

Taking these steps can help you avoid common pitfalls and maximize your policy’s benefits.

Are you a business with 20 or more employees looking for reliable cyber liability insurance? If your company is growing, you need protection that keeps up with your changing risks and requirements. We understand how important it is to have the right coverage in place to defend against cyber threats and financial losses.

Our team at MBPS specializes in helping businesses like yours find the best insurance solutions. We’ll guide you through the process, explain what cyber insurance covers, and make sure your policy meets all cyber insurance requirements. Contact us today to get started and protect your business from costly cyber incidents.

Cyber insurance for small business owners typically covers costs related to data breach response, such as customer notification and credit monitoring. It can also help pay for legal fees, regulatory fines, and restoring lost data after a cyber incident. Having this coverage protects your business from financial losses and helps you recover quickly from a breach.

The cost of cyber liability insurance depends on factors like your business size, industry, and the amount of sensitive data you handle. Insurance cost can also vary based on the level of coverage you choose and your history of past claims. Comparing different insurance policies can help you find the right balance between price and protection.

Cyber insurance is important because it fills gaps that traditional business insurance may not cover. With more businesses facing cyber threats and ransomware attacks, having dedicated cyber coverage ensures you’re protected against modern risks. This type of insurance can help you avoid major financial losses and keep your business running smoothly after a cyber event.

Cyber insurance requirements can vary by industry and client contracts. Some businesses need to meet certain cybersecurity standards or provide proof of regular employee training. Meeting these requirements not only helps you qualify for cyber insurance coverage but also reduces your overall cyber risk and improves your security posture.

Insurance for small businesses provides financial support to recover from cyber attacks, including covering the costs of hiring cybersecurity experts. It also helps with risk management by encouraging better security practices and offering resources to prevent future incidents. Having this coverage gives you peace of mind and helps you focus on growing your business.

Technology errors and omissions insurance protects businesses that provide technology services from claims related to mistakes or failures in their work. It is different from cyber liability insurance coverage, which focuses on losses from cyber incidents like data breaches. Some businesses need both types of insurance to fully protect against all technology-related risks.